A growing market for sustainable opportunities

GWI estimates that total global expenditure on sludge management will reach $15.5 billion in 2022, with this figure set to rise as populations grow and disposal routes dwindle. This is particularly felt in mature markets like Europe where regulations regarding disposal are becoming stricter.

Germany, for example, has put in place legislation that will ban land application of sludge as a disposal route from 2032 – following similar bans in place in the Netherlands and Switzerland. Emerging innovations in resource recovery technology, however, may open the door to offset sludge disposal costs by introducing a plethora of value-generating streams.

The biorefinery concept looks at the potential of redesigning sludge treatment plants to capitalise on such revenue streams. Instead of focusing on decreasing waste volumes, these plants could be meticulously engineered to maximise recovery of resources at every treatment stage. Taking inspiration from oil and petrochemical refineries, where processes are designed for maximum efficiency and the production of profitable end-products, biorefineries can use sewage as a feedstock to produce valuable products.

By bringing this resource recovery process into the treatment of sewage sludge, biorefineries can also support a move towards a circular economy, as recovered products can reduce the need for raw material production. While fully maximised resource recovery from sludge may still be a futuristic dream – captivating the minds of bioresource process engineers rather than the plans of the average utility – innovative technologies are already bringing many aspects of the biorefinery into reality.

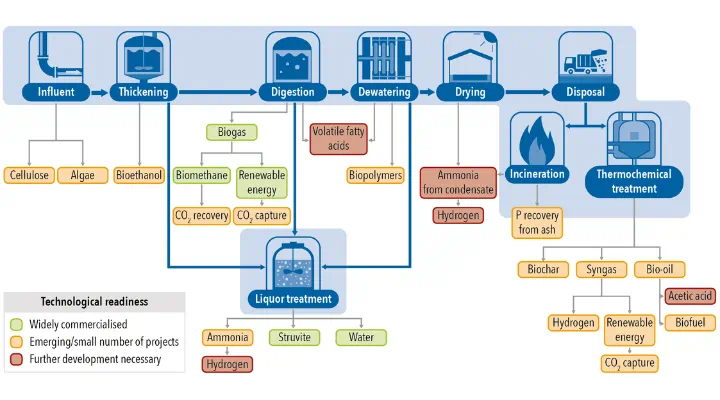

What resources can be recovered in a biorefinery?

Increasing emphasis on recycling and reusing waste materials is resulting in a greater appreciation of the resources they contain. Sewage sludge is full of potential for utilities, with many already extracting energy, phosphorus and nitrogen via anaerobic digestion and nutrient recovery processes, respectively. Tentative steps are being made into recovering biopolymers and producing hydrogen, and the recovery of volatile fatty acids and cellulose could become more viable in the future. Hence, the biorefinery concept could transform sludge management from a necessary cost to a valuable opportunity and offer a sustainable potential business model.

Source: GWI

As can be seen in the above graphic, there are many possible avenues for resource recovery from the treatment stream of sewage sludge. The level of market readiness of the technologies involved, however, varies significantly. Biogas capture from anaerobic digestion, for example, is widely commercialised as an energy generation process for both onsite use and export to national grids. One emerging market, with limited applications thus far but showing great potential, is ammonia recovery.

Reducing emissions and creating value with ammonia recovery

By recovering and reusing ammonia from sludge treatment, utilities can meet regulatory standards on nutrient pollution while generating an additional product. Furthermore, when ammonia is left in sludge, it releases the highly potent greenhouse gas of nitrous oxide (N2O), with ammonia recovery being an emerging strategy to mitigate these emissions. GWI models estimate that N2O released from sludge management accounts for 5.2 million tonnes of carbon-equivalent emissions globally each year; this represents 32 per cent of greenhouse gas emissions from sludge management.

Liquor and condensates from sludge treatment have high ammonia levels, with UK-based engineering company Atkins reporting that 2-3 per cent of the UK’s total ammonia production could be offset using recovery from sludge. The key technologies to achieve this recovery are chemical and thermal ammonia stripping, both of which can be applied in liquor treatment. Companies offering these solutions include Anaergia, Organics Group and Nijhuis Saur.

Once ammonia is recovered, the most established end-use is for fertiliser production, in place of ammonia produced through the dominant yet fossil-fuel dependent Haber-Bosch process. This highly ammonia-demanding industry presents the opportunity for two-fold emissions reductions: replacing a carbon-intensive new material with an emissions-reducing recycled material.

Shifting perspectives on agricultural spreading

Given the high nutrient value of sludge, it comes as no surprise that ammonia recovery isn’t the sole contribution sludge plants can make to the fertiliser industry. Agricultural spreading of sludge is a common disposal method, providing a profit-generating route while providing farmers with a fertiliser option that is significantly less expensive than synthetic fertilisers.

This disposal route is generally available to sludge that has been put through digestion for stabilisation to reduce pathogens and odours, creating spreadable digestate. In the UK, for example, over 90 per cent of sewage sludge disposed of is recycled to farmland, according to the regulator Ofwat. This practice is also dominant in Spain, Australia and China.

However, concerns over the high potential concentration of nutrients, heavy metals and emerging contaminants (such as PFAS, microplastics and pharmaceuticals) in digestate are impacting the availability of agriculture spreading as a disposal route. This can be seen in Switzerland and the Netherlands, where legislation currently bans spreading digestate to land.

Similarly, Germany’s 2017 Sewage Sludge Ordinance will come into force in 2032, banning land application from plants over 50,000 population equivalent. While standards ensuring sludge quality for spreading exist in some countries – for example, via the Biosolid Assurance Scheme in the UK and EPA biosolid standards in the USA – uncertainty remains over the future of digestate spreading.

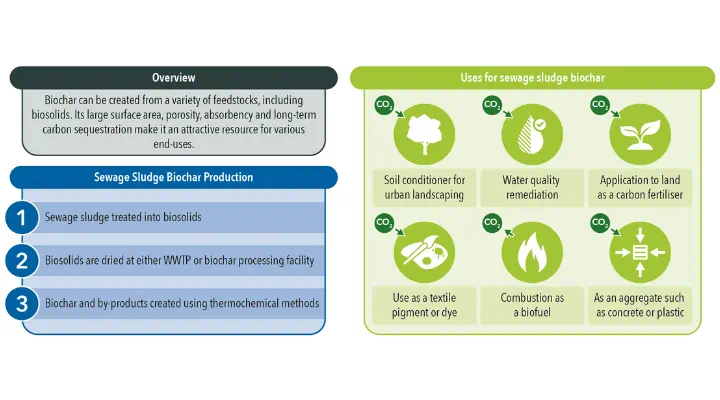

Biochar: one to watch

One digestate alternative gaining traction is biochar. Biochar is a high-carbon solid produced by the thermochemical treatment of sludge, using processes of pyrolysis or gasification. This high-heat treatment has been shown to remove PFAS and other contaminants of concern from the resulting biochar.

Additionally, biochar fertilisers are not water-soluble, and nutrients are released slowly, thus limiting eutrophication concerns linked to agricultural nutrient leakage into surface waters. This high stability further increases the appeal for biochar fertilisers, as their efficacy is measured in centuries – compared to weeks of efficacy for synthetically produced fertilisers. Finally, biochar serves as a stable form of carbon sequestration, thereby supporting the Net Zero carbon emissions targets being set by a growing number of utilities.

Source: GWI

The biochar market is still emerging, however. A plethora of alternate uses for the product are being researched, while companies including Anaergia, Kore Infrastructure, Pyreg and Aqua Green lead the market for biochar fertilisers. Furthermore, regulatory barriers such as the EU Fertiliser Regulation, which was updated in July 2022 and excludes sewage sludge as an acceptable feedstock for biochar fertilisers, currently limits the scope of the market.

Some EU member states – including the Czech Republic, Denmark, and Sweden – have taken matters into their own hands recently by introducing country-level regulation which allows sewage sludge biochar to enter fertiliser markets. Additionally, the industry standard organisation European Biochar Certificate is conducting a review which may see sewage sludge included as an approved fertiliser feedstock; this move may prompt wider EU-level change. If and when the legislative landscape shifts to better support sewage sludge biochar, there may be significant potential for growth.

A path towards a future circular economy

Along with legislative support, as highlighted, technological development is still needed for many of the resources within sludge to be recovered effectively. For example, volatile fatty acids are beginning to raise excitement in the industry, but recovery processes have yet to be demonstrated. Growing enthusiasm for circular economy principles is however encouraging this research and development into how such resources can be transformed into value again. This can be seen in funding opportunities like Ofwat’s Innovation Fund and the EU’s Horizon Europe fund which are available to support early-stage adoption of sustainable emerging technologies.

As technological development is achieved and the water sector implements such innovative solutions, there is scope for significant value-generation to occur in the coming decade. While change is likely to be gradual, the biorefinery could demonstrate the opportunity to fully incorporate circular economy principles into the wastewater sector and close the resource loop by minimising wasted materials.